Randy’s 2025 Financial Plan of a Lifetime.

23 years. Retire. Invest. Spend. This is how I did it. And, maybe more importantly, how I’m doing it.

My most important and popular post of the year.

My Plan.

This is MY plan. I took the best ideas I could find, mixed them, and matched them to make MY plan. I rarely come up with any of my own ideas. However, I am very adept at taking other people’s ideas and making a plan for myself.

I have been very successful in retirement. How do I define success? From a monetary point of view, I only wanted to achieve two things.

- Provide for my wife and children.

- Be able to afford a lifestyle that would allow me to travel the world constantly without a financial care in the world.

I am happy to report that my Financial Plan of a Lifetimehas allowed me to achieve both of these monetary retirement goals.

23 years of financial results.

I’ve been retired for 23 years. This is my 23rd annual review of my retirement financial plan. As measured by my net worth statement, I have more money today than I did 23 years ago. Later, I will explain why the previous statement indicates a major FAILURE in my retirement plan.

I’ve been telling people about my plan every year for 23 years now. Much of what I share in 2025 is the same as what I shared in 2024 and for the years before that. Why is that?

I’ve had a good plan from the beginning! I’ve made some minor tweaks, but only minor tweaks. However, when I tell you how I did it, I’m reinforcing to myself why my Financial Plan of a Lifetime is such a good one.

Please don’t mistake my confidence for bragging. To put it simply, I am sharing PEARLS with you. All you have to do is bend over to pick them up. Then, and this is most important. You will have to put these pearls in your own piece of jewelry. Look for the “Pearl” designation throughout my post in RED.

No matter what your age this plan works.

If you are in your 20s or 30s, you might think, “This is just some old guy trying to brag about how he planned for retirement. That doesn’t have much to do with my world. I won’t be retiring for decades. I don’t need to give this topic much thought right now.”

If you are in your 40s or 50s, you might say, “Hold on. I haven’t been giving these financial reviews all that much attention. But now, just over the horizon, I can see retirement for myself. Maybe I should pay more attention to how Randy did it.”

If you are in your 60s or older, you have likely initiated your financial plan….or not. If that is the case, you can compare your thoughts on retirement financial planning to how I did it. Maybe you didn’t have a plan? Surprise! You DID have a plan all along. What was your plan? No plan!

My most popular newsletter.

This is my most popular newsletter of the year. I get the most reader responses and questions from this post. I hope you enjoy it.

Based on what we all learned when we were five years old, everyone thinks about money differently. Few people can change how they feel about money, even if they don’t know how to manage money at all. Not being able to change is a bit sad, but it is a reality in so many cases.

It seems a bit weird to me that how we feel about money is something we learned as small children. That thinking comes from everything I’ve read. It seems even more bizarre to me that people who don’t understand money wouldn’t take a plan like mine, or at least SOMEBODY’S plan and run with it! I’m thinking that most people don’t understand that they don’t really understand how to manage money.

This situation is similar to when people are asked if they are above-average drivers. About 75% say they are above average. Of course, we all know that can’t be true. Most people are not above average with money either.

There’s an excellent chance you think about money differently than I do. That’s OK. I’m just sharing with you in a most candid manner exactly how I did it. I hope you find what I have to share entertaining. Maybe you’ll find what I have to share educational. Perhaps you’ll find what I share so counter to your thoughts on money that you will have a hard time reading everything posted here.

Different strokes for different folks? No, I don’t believe in that. Some things in life, if done the best way, yield significantly different and, most importantly, better results.

I was born in 1949. We were poor. Luckily, we didn’t KNOW we were poor. That made being poor easier!

The year 1949 was a long time ago. Heck, 2002, when I retired, was a long time ago. In 1949, cars didn’t have air-conditioning, power windows, or self-driving capability. Even AM radios were an option in 1949. In 2002, there were no Teslas, iPhones, YouTube, or Facebook. 2002 was about as long ago as 1949!

Why did I retire?

I retired at the age of 52. I wanted to retire much earlier, but things just got in the way of making that a reality.

Why did I retire? I was the kind of guy who liked to play more than work. I wanted to do a good job when I worked, and I did. As I thought about retiring, this thought was at the front of my mind. “If out of the infinite number of things I could do with my time, working for Procter & Gamble was #1, then I shouldn’t retire. However, if I had the money and didn’t need to work, I might as well spend my time doing exactly what I wanted, and working for a big company wasn’t that.”

I always means we…and it’s just shorter to write.

You will often hear me use the word “I” in this message. I don’t want you to get the wrong impression. Some time ago, I married a beautiful young blonde girl named Carol. Carol and I did all of this together.

I will tend to use “I” in my description of my retirement financial plan because I am the money man in our household. Carol is the “everything else” woman.

What does that mean? I handle the financial strategy. Carol pays the bills. Carol is responsible for everything else that goes on in our household. She does everything!

I’m not lazy, just focused.

I’ve told you that I don’t do any chores at home. I last mowed a blade of grass in 1983. I will never mow another blade of grass in my life. That’s a promise. I don’t wash dishes or clothes. I don’t know what day of the week the trash man comes or when the cleaning lady is scheduled to show up. I don’t worry about knowing anything that I don’t NEED to know.

It is essential for the reader not to take anything that I say out of context. I am not some chauvinist unwilling to support how a typical household must be run.

I am simply unqualified. Unqualified people should not attempt tasks for which they are incompetent.

The infamous job jar.

Carol has attempted to involve me in these household chores and responsibilities. She even created a “job jar.” This girl doesn’t give up! In the job jar, there was a list of chores. She neatly arranged small papers, just like you might find in a Chinese fortune cookie.

Carol explained to me, as if she were a kindergarten teacher, that the job jar’s purpose was for me to reach in and grab one of these small papers. I should read my assignment and then complete the task. As I expected, this didn’t work well.

In an effort to be a good husband, I would reach into the jar and grab one of the “opportunities.” However, I couldn’t resist saying that I didn’t want to do what was described. As a loyal husband, I had to stick up for myself.

Occasionally, I would find something I thought I could do in the job jar and attempt to do that chore. Carol would look over my shoulder closely and soon tell me that my actions did not meet her standards. She would then redo what I had done to ensure the end result met her standards.

As you might understand, this was frustrating for me. Why would I want to waste my time doing a chore or executing a household responsibility if Carol was going to come right behind me and redo it? This is how we moved into the position we have been in for decades. I don’t do anything except handle the financial strategy.

The reader might ask themselves, “Randy, do you do this or do you do that?”. Folks, I don’t do anything. I’m not bragging. I’m simply telling you how it is. So, with that background, I say to you that I am fully responsible for our retirement financial plan. Carol agrees. She does not look over my shoulder regarding our financial retirement plan and try to redo my financial strategy. She is an intelligent woman. She knows that, just like with Allstate, she is in good hands.

When I quit…I quit.

I have never worked for anybody else in retirement or earned a single dime of work income in more than 23 years during retirement. I don’t need to work, and more importantly, I don’t want to work for money. Some folks say they love their jobs. I would love to hear what those people would say if their job stopped paying them money.

Let’s consider this. When I decided to retire in 2002, I had a certain amount of money. Now, I have quite a bit more than I had in 2002.

How did I get in this position?

How in the world did that happen? I haven’t worked in retirement. We have yet to receive any money from anyone else to build this increasing net worth. Carol never worked outside the home for money or any other reason after our daughter Kristy was born (above!). To avoid revealing Kristy’s age, I will tell you that Carol hasn’t worked outside the home for money for more than four decades. Don’t get me wrong. What Carol did for our family was much more important than what I did in business. It’s just that in our world, what I was doing produced more income.

In this post, I will tell you precisely what my Financial Plan of a Lifetime was and the results I have achieved so far. However, if you’ve been reading my newsletter for long, you know I always try to provide a little background. When doing that, sometimes my message is not always a short read. You expect to learn how to earn hundreds of thousands of dollars by reading three paragraphs?

Nevertheless, so many readers open these messages every couple of weeks, hoping to get a chuckle or a piece of information that might be valuable to them, their family, or their friends. And they do!

What will your reaction be to what I’m sharing?

I always say that everyone can choose their reaction to whatever they encounter. Everyone can decide whether they want to react positively to the information that comes their way.

What is your reaction when I tell you this? I retired 23 years ago. I’ve been spending like a drunken sailor ever since. I never earned any income whatsoever from work during that time. I have more money now than I did when I retired. What is your reaction to all of that?

In my judgment, I would find it perfectly acceptable if you concluded, “Randy is a financial stud.”

Others might say, “Randy likes to brag”.

If you had either of these reactions and you were willing to share them with me, this is what I would tell you.

Dizzy Dean had it figured out.

If you are in your 20s, you probably don’t know who Dizzy Dean was. Dizzy Dean was a phenomenal young pitcher from Arkansas who played for the St. Louis Cardinals. He was so good that he is in the Baseball Hall of Fame in Cooperstown, New York.

Later, he became a TV broadcaster on the Major League Baseball “Game of the Week.” Ol’ Diz was a country boy. He was fond of saying, “It ain’t braggin’ if you did it or you can do it.” I have done precisely what I am telling you I did. I always follow Dizzy Dean’s adage, “It ain’t bragging if you did it.”

You may have heard other people tell you something similar to my story. They might say they retired long ago and have more money today than when they retired. If you know one of those people or you ARE one of these people, you might think that person WAS a financial stud. I will tell you this.

Pearl! It is easy to make this mistake. Don’t do it. Enjoy your money.

I am not bragging; I am NOT a financial stud. Anybody who tells you that they retired a long time ago and have more money today than when they retired has made an enormous mistake. If they don’t realize that, then they have made TWO mistakes.

People in this situation have optimized for money more than they should have. They worked too long or didn’t spend enough of their money in retirement. That’s right. They optimized for money and not for personal enjoyment. Money, by itself, isn’t worth anything. If you have more money after a certain number of retirement years than when you retired, in my judgment, you have FAILED!

I have failed…but it’s not too late.

This is not a message about you. It is a message about me. From a financial standpoint, I have failed. I’ll bet you didn’t see that coming.

That’s right. When you hear me say that I have more money today than when I retired 23 years ago, don’t think I am bragging or a financial stud. You should think, “Randy is failing.”

Maybe you think Randy cut back on his expenses so much after he quit working that there was no fun to be had. Read on. Decide for yourself.

Pearl. Limiting your spending does not usually optimize for personal enjoyment.

One way someone could achieve what I have done is to severely limit their spending in retirement. I didn’t want to do that. If I were going to retire, I would have a lot of free time. If I were to have a lot of free time, I would likely need something to entertain myself. Filling my free time would be expensive.

I wanted to spend like a drunken sailor.

My objective in retirement was to spend money like a drunken sailor. Wait! When have you ever read about a retirement financial strategy where the author told you that he or she wanted to spend like a drunken sailor?

I wanted to travel, have nice things, and play golf with the guys down at the club. That’s a much different lifestyle than living in a van down by the river.

At this point, the word “I“ really does apply to me and not so much to Carol. Carol is not interested in spending like a drunken sailor. She doesn’t even drink that much.

If Carol weren’t married to me, she might never travel. Believe it or not, she still does her household chores wearing clothes that she wore in college. I am not exaggerating. What does that tell you? First, she don’t eat much. She can still fit into the clothes she wore in college! She works out at the gym several times a week. Carol would be just as happy doing all of her chores at home and never stepping onto an airplane. I don’t roll that way. Because I don’t roll that way, she don’t exactly roll that way either.

Bigger is better, in my judgment.

When we retired in 2002, we bought a new house. Did we downsize? No, we did not. That’s not my style. I don’t believe in downsizing anything in retirement. I went big. I built an indoor basketball court about the same size as my boyhood home, where I lived for the first 15 years of my life.

Was this house going to be our forever house? Not exactly. We paid $1.2 million for it. Think about that for a second. In 2002, we spent more than $1 million on a house. It must’ve been some house, huh? How much is $1.2 million worth in today’s dollars? Dollartimes.com will tell you that 1.2 million dollars in 2002 is worth well over TWO million in 2025.

What was the first thing we did with the house we bought at the beginning of retirement? We tore it down. That’s right. I guess that house wasn’t our “forever” house, was it?. We could have just changed the wallpaper, but we tore it down. That house caused me to do one of my rare household chores.

![]()

I learned to swing a pickax.

I went to Home Depot and bought just one item—a pickax. I would go down to the new house with the objective of totally destroying one room a day with my pickax. It was fun. It would be best if you didn’t get the impression that I enjoy doing chores, but this one wasn’t that bad.

In no time, I had torn down the house to the studs. Then, I discovered the house had about an inch and a half of “light concrete” on all the floors. The bathroom showers and such were constructed in the same way that 1950s bomb shelters were. They were all REINFORCED. Concrete and rebar. I needed some help.

Meeting these folks was a trip.

I came across a minister who ran a shelter for people who needed rehab from drugs and alcohol. To this day, I don’t remember how I met this guy. I told the minister he could keep all the wood and anything else of value he found in the house if his guys helped me destroy our million-dollar mansion.

I worked side-by-side with these folks. Boy, did they have the stories to tell. They had been in jail. They had lived on the “wild side of life.” I’ve never even taken a puff of a cigarette. It was entertaining to go down every day and listen to their stories.

We hauled the debris we created in this multi-level structure up to the top level in massive, hard plastic trash cans. Soon, all this debris was so heavy that I was told to remove it before the floor collapsed. I rented a full-sized dump truck and made six trips to the dump in one day, driving that truck at about 30 mph on the San Diego freeway.

The house was now a shell of its former self. I hired a guy to do the final demolition. He did that demo in one day. When we negotiated the demolition price, we ended up being $700 apart. I suggested we flip a coin for that final $700. The demo guy agreed. We flipped a coin. I won. He did that demo pretty cheaply. Folks, that’s how I roll.

I tore that house down and built a new one.

When it came time to build the new house, I spent another $1.2 million on its construction. I spent $2.4 million (buying the first house, tearing it down, and building a new one) on this retirement home in total in 2002.

How much was our total construction cost of $2.4 million worth in today’s dollars? Dollartimes.com will tell you that $2.4 million in 2002 is worth more than FOUR million dollars in 2025. Oh yeah, we didn’t sell the house we lived in at the time. Why? We couldn’t. No buyers. That put a little “pucker” into the subject of cash flow.

I hired a construction consultant for, as I remember, $80,000. He shared all of his construction knowledge and contacts with me. We ended up with 80 subcontractors, and several of them had subcontractors below them. I’ll call our construction consultant, Matt, because that was his name.

Along the way, we hired a woman to be our “space planner”. She was wonderful. I’ll call our space planner/designer Patty again because that’s her name.

If Matt had been left to his own devices, he would have built a tank. If Patty had been left to her own devices, she would have given us a beautiful butterfly that flew around on an unlimited budget. You can imagine the meetings that Matt, Patty, Carol, and I had in building our forever home.

How many door hinges should a house have?

I call our home our “modest seaside cottage”. What did $1.2 million in construction costs get us in 2002? I think our house has 33 doors. I haven’t been in all the rooms yet. The doors were the best value in the house. They are solid Honduran mahogany. Each door needed three hinges, so we needed nearly 100 door hinges in total.

I told you I grew up poor. I know you’re not going to believe this, but I grew up in a small home at 411 Doering in East Peoria, Illinois. I lived in this house until I was fifteen. The house had 990 square feet.

How many doors did that house have? To the very best of my memory, it had three doors. There was the front door, which we never EVER used. There was the back door, which we used to enter the house. Finally, a door separated my room from the home’s one bathroom. Three doors. Nine hinges. Times have changed.

The cost estimate for each hinge for our new home ranged from $6 to $24. We had to decide whether to go with the low, medium, or high bids with each of our subcontractors. It’s rare for me to cheap out. For the door hinges, the contractors made it sound like the six-dollar door hinges would probably rust away in the first five years of occupancy. Then, those solid doors would fall over onto the floor. On the other hand, the $24 hinges were made to sound as if they were made of pure gold. Did we want to spend $600 on hinges or $2,400?

We made decisions like these with all 80 of our subcontractors. Most of the time, we went with the high bid and better quality over the low bid. I was practicing spending like a drunken sailor!

Oh yeah, we used cash discounts extensively. What a huge money saver that was. It was just fun being part of those negotiations. I wish I could tell you more about the winter night when I ventured into a bad part of town with a Hartman briefcase carrying $63,000….in cash, but I can’t. Details on that subject might be forthcoming, but likely not, in a future newsletter.

Pearl. We optimized for personal enjoyment.

We spent a lot of money on our house. I also told you that I wanted to travel a lot in retirement. I’ve done that. Carol and I have been to 102 countries. Yes, I played a lot of golf as well. The lowest I ever got my golf index was 3.2. That’s another story for another time as well.

A friend sent me this note. I thought it made perfect sense. This is what it said.

“Don’t be afraid to spend money on traveling. Be afraid of growing old and realizing that the only place you ever went was to work.”

I’ve been to more than 20 countries, most of which were return visits, just in 2025.

Pearl. My pre-retirement spreadsheet was my financial bible.

This is really important. I have a spreadsheet for everything. I attribute my pre-retirement spreadsheet for allowing me to pull the pin on retirement. I often think back on what might have happened if I had screwed up a formula in that spreadsheet. It was that kind of planning that allowed us to achieve financial success.

How much would come in and how much would go out.

The spreadsheet told me roughly how much my investments would earn in retirement. The spreadsheet told me roughly how much my expenses would be in retirement…for the rest of my life.

I wanted to travel. I may go overboard on travel. My goal is to take the “trip of a lifetime” every month, and I pretty much do.

I wanted to spend the money I had earned. Having my retirement money sitting in a Vanguard retirement account while I aged, sitting in a La-Z-Boy recliner watching TV, wasn’t part of my retirement plan. I have no idea how long I will live in retirement. I can tell you this. I’ve been busy in the first 23 years of my retirement!

The table below shows the number of nights that I have traveled away from home since retirement.

| TOTAL | 3,757 |

| 2025

2024 |

More than 200 so far!

181 |

| 2023 | 162 |

| 2022 | 181 |

| 2021 | 129 |

| 2020 | 115 |

| 2019 | 166 |

| 2018 | 213 |

| 2017 | 171 |

| 2016 | 186 |

| 2015 | 194 |

| 2014 | 189 |

| 2013 | 186 |

| 2012 | 142 |

| 2011 | 162 |

| 2010 | 159 |

| 2009 | 167 |

| 2008 | 162 |

| 2007 | 146 |

| 2006 | 160 |

| 2005 | 163 |

| 2004 | 143 |

| 2003 | 80 |

As you can see, I have averaged 165 nights of travel each year for 23 years. In 2018, I spent 213 nights on the road. I’m pretty sure I will break my all-time record in 2025. I am a “road warrior”. I like to travel.

Considering each of those travel days, I would like you to think about this. On 99% of those more than 3,700 days, I needed a hotel. On 99% of those days, I needed a rental car. On 99% of those days, I bought two or three meals in a restaurant. About every third or fourth day, I flew on an airplane.

I have parked my car at the Los Angeles International Airport for over 4,000 days during retirement. As you can imagine, we have spent some money on travel. Remember, I have not earned any money whatsoever from working for more than 23 years in retirement.

Speaking of spending money, I like driving brand new luxury cars. I was driving new Lexus automobiles when I retired. Six years ago, I decided that electric cars were the way to go for me. In 2019, I took delivery of my first $100,000 automobile, a Tesla Model X.

What does all of this prove?

I share the above regarding the cost of our housing, travel, and automobiles to prove one point. We didn’t get to where our net worth is greater today than 23 years ago by skimping on expenses. I literally did spend like a drunken sailor!

Now let’s get serious.

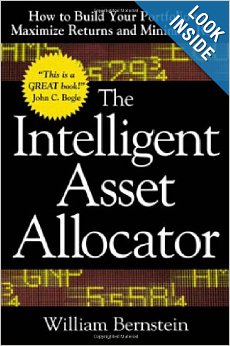

We got there by having a solid financial plan. I started with William J. Bernstein’s book, The Intelligent Asset Allocator: How to Build Your Portfolio to Maximize Returns and Minimize Risk.

I read it, but more importantly, I practiced what the book advocated daily. The author taught me the value of having a diversified portfolio of stocks and bonds in retirement and the importance of never timing the market. I planned to invest in low-cost index mutual funds. When I did that, I was nearly guaranteed to achieve the market’s average results. I would be able to match the market.

I avoided financial planners (like the plague) who charged a percentage of my assets as their fee. “Being the market” by simply being “average” was good enough to beat 90% of active investors and those who followed the recommendations of financial planners.

Pearl. Make a plan. Stick to the plan. Change the plan only if absolutely necessary.

I have not deviated from my financial plan one iota since 2002. I don’t know if Dizzy Dean said this, but he could have: “If it ain’t broke, don’t waste time fixing it.”

I still have the same eleven Vanguard mutual funds I had when I retired. Nothing else. My plan didn’t have to be done with Vanguard. Other major investment management companies offer similar products.

![]()

What were those funds?

| Total Stock Market Index Fund Admiral | VTSAX |

| Total International Stock Index Fund | VTIAX |

| U.S. Growth Fund Admiral Shares | VWUAX |

| Windsor II Fund Admiral | VWNAX |

| Strategic Equity | VSEQX |

| Explorer Fund Admiral | VEXRX |

| Short-Term Investment-Grade Fund Admiral | VFSUX |

| Short-Term Bond Index Fund Admiral | VBIRX |

| Intermediate-Term Investment-Grade Fund Admiral | VFIDX |

| Long-Term Bond Index | VBLAX |

| High-Yield Corporate Fund Admiral | VWEAX |

I mentioned that when I retired, I created a financial spreadsheet. That spreadsheet included just two essential items. It helped me understand my expenses and my expected investment income in retirement.

Pearl. Don’t have a budget? Sorry to hear that.

A household budget has always been a critical first step in my financial planning. Some might call their budget a “financial tracking” tool. I do. I use this tool about 20% of the time to look back and about 80% of the time to look forward. Did you get that? The time I spend on financial tracking is used mainly to look into the future.

The year before I retired, I knew how much I was spending in 10-15 different expense categories. My spreadsheet also included another essential element: For each expense category, I made an educated guess on the amount of inflation by category for the next year and every year into the future.

I can tell you how much each of our expenses will be by category within a fairly narrow range in 2030, 2040, and beyond. The challenge will be to live long enough to prove those projections!

I could tell you how much our electric bill will be in the future. Wait. That’s a bad example. We have solar panels, and our electric bill is zero. How about this example? I can tell you how much our gasoline expenses will be in the future. Wait. That’s a bad example. I drive a Tesla, and my gasoline expense AND my cost to charge my car is zero…but you get the point.

A budget for all times.

This is my kind of budget. Looking back, a budget is a factual document. Looking forward, a budget is an educated estimate. If a person doesn’t have a budget, they won’t know where they’re at or where they’re going. I once read a book titled “If you don’t know where you’re going, you might end up there”. A budget/financial tracking tool is the basic building block of a sound financial plan.

My budget tells me how much I have spent and, more importantly, how much I expect to spend.

When I decided to retire, I needed to look at how much money I had at the start of retirement. I thought I had enough to retire for the rest of my life and never work again. I told my bosses to “take this job and shove it”. Not really, but that does sound kind of cool, huh? What if my future projections had been wrong? Had I been wrong, it’s unlikely you would be reading this newsletter.

Based on my homemade spreadsheet, I submitted my retirement papers and told the folks they could reach me at the beach. Yes, we live at the beach.

Pearl. How much would I earn on my investments?

With some historical research, I estimated a reasonable rate of return I could earn on my retirement assets. Of course, those rates of return would be different every year. There would be ups and downs.

I didn’t expect a global financial crisis or a global pandemic during my 23 years of retirement. Stuff like that is hard to predict, but it’s not surprising when it happens. Bumps in the road will always be there.

October 11.

My fiscal year ends every October 11. Why October 11? When I retired on June 30, 2002, it took me until October 11, 2002, to implement my financial plan.

Pearl. This year’s results.

The bottom line!

For my 2024/2025 fiscal year ending October 11, 2025, my retirement portfolio earned 13.2% percent. That’s an excellent result. The annualized ROI for my entire 23 years of investing is now 8.8%. That’s about what should be expected from an almost all-index portfolio of 64% stocks and 36% bonds.

The table below shows my return on investment (ROI) for each of the past 23 years. I use the Modified Dietz method to calculate my ROI. My portfolio has a 64% stock allocation and a 36% bond allocation. There have been only two losing years in my 23 years of investing.

Monday morning quarterback.

I had one guy tell me I would have made a lot more if I hadn’t invested in bonds and had put all my money in stocks. First, that is true. But the bonds provided some stability during the global financial crisis and when the market cratered temporarily at the beginning of COVID-19.

These are my annual investment results for my entire retirement portfolio by year.

| FY ENDING | ANNUAL ROI | ANNUALIZED ROI |

| 2003 | 22.85% | 22.9% |

| 2004 | 10.30% | 16.4% |

| 2005 | 9.58% | 14.1% |

| 2006 | 11.44% | 13.4% |

| 2007 | 15.89% | 13.9% |

| 2008 | -24.05% | 6.5% |

| 2009 | 24.58% | 8.9% |

| 2010 | 4.10% | 8.3% |

| 2011 | 1.30% | 7.5% |

| 2012 | 11.00% | 7.8% |

| 2013 | 15.27% | 8.5% |

| 2014 | 5.00% | 8.2% |

| 2015 | 5.70% | 8.0% |

| 2016 | 5.50% | 7.8% |

| 2017 | 15.41% | 8.3% |

| 2018 | 4.33% | 8.1% |

| 2019 | 8.46% | 8.1% |

| 2020 | 16.91% | 8.6% |

| 2021 | 21.26% | 9.2% |

| 2022 | -18.61% | 7.6% |

| 2023 | 14.90% | 7.9% |

| 2024 | 22.80% |

8.6%

|

| 2025 | 13.19% |

8.8%

|

I’m glad I didn’t listen to those people telling me five or ten years ago that the market had been doing so well that it would level off. They said returns in the future would be “below average” for a long time. There is one thing I have learned about predictions regarding stock market returns. The predictor has a 50% chance of being right! Stocks and bonds will either go up or down during the predictor’s time frame. I make only one prediction about the market. The market WILL go both up and down!

Pearl. I am not a market timer.

If I had listened to people like that and bailed, I would have been a market timer. I am not a market timer. I don’t move in and out of the market based on hunches or advice from a financial planner. I don’t move in and out of the market based on my hunches. I stay the course. Please reread the last sentence. I stay the course.

I had a friend who drove Cadillacs and owned his own company. He would tell me he could “feel” when the market was getting ready to take a dive. Luckily, I valued his friendship and bit my tongue. His logic sounded like so much horseshit. It did make me think about him a bit differently than when he told me that in the future.

Pearl. I have never paid for investment advice.

I have never sought the advice of a financial planner to pick investments. I use people like that for estate planning, taxes, and other related tasks. I have never paid a financial planner a single penny for advice on which investments to choose or whether to be in or out of the market. My financial plan is super simple. I don’t buy individual stocks based on a tip or my research. I have other hobbies.

Pearl. This is how I did it. This is how I am doing it.

This is me. This is important. I have eleven mutual funds, most of them low-cost index funds. I don’t time the market; my stuff is broadly diversified. I am comfortable with this because I know enough about long-term investing to be comfortable with the expected outcome.

A financial planner could be a good idea if someone doesn’t have a background in finance. I always tell people that when they get financial advice from anyone, they have to decide if that person stands to earn money by giving that advice. Quite often, they do.

I will take this adage to my grave. Don’t ask your barber if you need a haircut! Don’t ask anyone for advice if they stand to benefit from the advice they are giving you.

Pearl. Think you can beat the market?

You can’t. Just know that people have a tough time with this idea. It is EXTREMELY difficult to beat the market in the long run. If your financial planner tells you they can beat the market by enough to cover their fees and still give you a better-than-market return, you might ask them these questions. Can they guarantee that? Will they waive their fees if they DON’T beat the market? If you get a positive response to these questions, please share your financial planner’s phone number with me.

Pearl. Market timing is for suckers.

Some folks say the market has done well during my retirement years. I would agree. However, we did have a global financial crisis and a global pandemic. When those things happened, it would have been easy to step out of the market, potentially at the wrong time. Had I done that, I would have been a market-timer. A market timer has to be right twice. Once when they get out of the market and once when they get back in. I’m not smart enough to time the market once, let alone twice. Some people market time when they just KNOW what the future is going to be. Good luck with that.

In retirement, we’ve spent a lot of money and earned significant investment income. When I created that spreadsheet about our spending and potential retirement earnings expectations, I would have signed on the dotted line for an 8.8% annualized return over a long period, similar to what I’ve achieved over the past 23 years. That rate of return would have been good enough for me.

I work with arbitrage.

I told you that I have never worked for money since I retired. Some might disagree with that assessment. I have used various forms of arbitrage to create wealth. What is arbitrage? Is arbitrage magic?

Warren Buffett says you will never get rich working during the day. You get rich while you sleep. I believe in that 100%.

While I was sleeping, our home has appreciated significantly since we moved in. Home appreciation is a form of arbitrage. I built the house for $2.4 million and now have an interest-only mortgage for $2.558 million on the property.

Let’s stop here for just one moment. What bank in their right mind gives a guy who hasn’t earned a penny of work income in 23 years a mortgage for more than $2.5 million? Now, let’s continue.

What were these people thinking?

I’m as shocked as anyone that the bank would give me a mortgage for more than two and a half million dollars when I had no work income or job. They did that just four years ago. Was I shocked? I was not so shocked as to not submit a loan application…so there’s that.

Do the math. I picked a good location. We live just 100 yards from the white water of the Pacific Ocean. Our realtor always said, “All money flows to the sea.” I believe he was right about that.

Pearl. Interest only. That’s enough to pay these people.

I like interest-only home loans. My current loan carries an interest rate of 2.25% over a 10-year term. I’m four years into that term.

Just think about this for a minute.

Let’s think about that. If I had wanted to own my home free and clear, the bank would have my $2,558,000 now. Here’s the fun part of that interest-only loan. I have the friggin’ two and a half million!

My house would still appreciate the same amount regardless of whether I had a mortgage. With that being the case, I decided to invest that $2.558 million in the hopes of earning a higher return than the 2.25% home interest rate the bank was charging me.

How is that going? I would say pretty well. For the last four years, my investment rates of return have been (-18.6%), 14.9%, 22.8%, and now 13.2%. With those returns that $2,558,000 has now grown to $3,325,000. That’s a gain of $767,000. More than three-quarters of a million dollars in just four years!

All of that comes from investing the amount of my home mortgage and NOT giving that money to the bank, where those funds would be buried in the black hole of home equity, earning nothing. Folks, $767,000 is serious money!

During those four years, I paid the bank $230,000 in mortgage interest. The net gain of $537,000 ($767,000-$230,000) is a pretty nice piece of change for having an interest-only loan and investing the proceeds that were NOT given to the bank to achieve a mortgage-free home. Given all of this data, do you still think it’s best not to have a mortgage on your home?

Let’s say that in the first four years of getting that home loan, my investments did not outperform the interest rate on my mortgage of 2.25%. What then? I would still have control of more than $2.5 million to use as needed. I would also have that money in place when the market provided better, more expected long-term returns.

Oh, yeah…a couple more things. With my last refinance of the $2,558,000 loan, the bank gave me $300,000 in cash to spend as I liked. Yes, crazy! Well, it wasn’t exactly cash. They sent me a check! I cashed that check within an hour of receiving it!

I can take $30,000 a year from that money and do so for about 15 years, with investment growth, before that bucket of funds goes to zero. I can do a lot of traveling with 30 grand a year.

Finally, in four years, my mortgage loan (the IRS limits the mortgage interest deduction to just $1 million of the loan amount each year) has thrown off $90,000 in tax deductions. Those deductions have reduced my taxes (31% tax rate) by about $28,000.

I’ve used the same principle with my car loans since 2019. Borrow at low rates and invest in the market at rates of return far north of my car loan rates.

Pearl. How about some more arbitrage?

One last arbitrage item for me. I practice credit card arbitrage. Credit cards offer sign-up bonuses. They might give me 100,000 points if I spend something like $5,000 on their card in three months. I don’t charge anything on the card that I wouldn’t have bought anyway. We pay our bill in full each month. Each 100,000 points I earn is worth about $3,000 in travel expense reduction to me. We currently have 23 different credit cards and are looking for more.

Why do credit card issuers seek new business this way? Because some people will get that new card, charge lots of stuff, and not pay their bill in full each month! The credit card folks love people like that. I do too. If the credit card companies couldn’t count on those deadbeats, I couldn’t get those bonuses!

I charge everything humanly possible to charge on a credit card. Everything? I’m talking about federal and state income taxes and real estate taxes. I’m talking about insurance premiums and trips to McDonald’s when my bill for an ice cream cone might be $1.99.

I earn travel rebates that reduce my airfare and hotel expenses. As an example, if the best rate I can find on a Hyatt Hotel is $200/night, I use my credit card arbitrage earnings and points to bring that hotel expense to zero. In 2024, I earned $92,300 in pre-tax travel rewards. That’s serious money! I don’t have to spend those rewards in a single year. I don’t even have to spend these rewards on myself. I can give them to whoever I want.

Money is coming in from all directions.

As you can see, we don’t skimp on spending. My stock and bond portfolio is throwing off a 23-year annualized rate of return of 8.8%. My use of arbitrage with our home and car loans, along with credit card arbitrage, is earning gigantic amounts of money —nearly one million dollars in four years.

Arbitrage works best with low-interest loans. I’ve had low-interest loans for years and will have them on our house and car for many more. Yes, current interest rates are up. However, I’ve been sharing my low-interest loans strategies for years with anyone willing to listen. You snooze, you lose.

Pearl. Not my ideas.

I’m not that smart. I didn’t think of all of this on my own. But I am smart enough to see and run with a good idea from someone else!

I rarely have an original idea. However, I pride myself on taking other people’s ideas and applying them to my situation. William Bernstein inspired me to decide how to create a retirement stock and bond portfolio. I am indebted to Mr. Bernstein. I bounce my ideas off my son and good friends.

Pearl. This might be my favorite idea of all.

I am also indebted to a fellow by the name of Bill Perkins, who wrote a book called Die with Zero. I only discovered his book a couple of years ago. When I read it, I knew I had been practicing “Die with Zero” most of my life.

I can see people roll their eyes when I tell them the book’s title, “Die with Zero”. The book doesn’t recommend trying to die with no money! The author advocates optimizing for personal enjoyment rather than for money. If anyone reading this thinks I am trying to optimize for money, they have entirely missed the point. I am trying to optimize for personal enjoyment by managing money well.

Perkins recommends creating lasting memory dividends with your money. Nevertheless, people don’t want to hear that. They want to keep their money in the bank or an investment account. Why? People don’t like to change. That’s on them.

I strongly believe in exploring new ideas. When a better idea comes along, I will switch in a heartbeat. I don’t practice that theory in marriage, though! Of course, I have never had to consider a better marital idea because none has ever come along. A better marital idea for me doesn’t exist! I needed to put that last part in just in case Carol reads this far.

The Die with Zero concept was not new to me, but the label was.

I have been using the principles of Die with Zero pretty much all my life. Long before I retired, our family traveled their butts off. I earned 500 frequent flyer airline tickets while I was working. 500! Just to be clear, I am not exaggerating. People who know me know that I am not a guy who exaggerates.

When the family traveled, I was frequently upgraded to first class on airplanes. When that happened, I NEVER rode up front. We always had a method of getting Carol or one of the kids into first class.

I have always spent a lot of money on houses, cars, and travel. I wanted to optimize for personal enjoyment and not for money. Money unspent isn’t worth much. Money held until you are too old to enjoy it isn’t worth much.

In 1980, I was 31 years old. I bought a brand new 1980 fire engine red Cadillac Sedan Deville. I was optimizing for personal enjoyment. Sadly, that Caddie was the worst car I ever bought! Additionally, my boss drove a beat-up little bitty Honda hatchback. There were many days when our two cars were parked right next to each other at work. That might not have been my most brilliant corporate political move…but he took it pretty well.

Carol and I have lived in our current house longer than we have in any other place. During my business career, we lived in Peoria, Illinois; Fairfield, Ohio; Phoenix, Arizona; Mission Viejo, California; Ridgefield, Connecticut; Inverness, Illinois; and Laguna Niguel, California. We are now in our second house in San Clemente, California.

In each location, we stretched to get the biggest and best house we could afford. Why do that? We wanted to be comfortable. They say you gotta spend money to make money. They also say the cheap man pays the most. I love that last one. It’s so true.

Pearl. Location = appreciation.

Today, our home is worth nearly three times more than we paid for it. Location, location, location. When a relatively small number, $2.4 million, grows by nearly three times, you’ve got a much bigger number. You feel me, right?

Pearl. All I ever wanted from this was to be average.

There is nothing wrong with being average. When I retired, I was not shooting for nor expecting superior financial results with my stock and bond low-cost index mutual funds. I only wanted to be “average”. I just wanted to match the market. I figured the only way I could match the market was to be the market. After reading several investing books, I strongly believe that virtually no one beats the market.

We were lucky to spend much of our retirement in a low-interest-rate environment. As I recall, our construction loan was in the 3% range.

Did I tell you that it took 11 months to do the architectural planning for our house? It took 18 months to build the house. That’s 29 months. On the day we moved in to take advantage of our home loan terms, we didn’t have a front door. All we had was a massive piece of carpet covering the open space. Carol didn’t like that in a big way. All I could say to her is that I never try to tell her how to manage her stuff. We got through it.

Pearl. Refinance. Refinance. Refinance.

Refinancing your home is a slog. It’s not fun. I always say a refinance is never done…until it’s done. It’s more fun to play golf and travel than to refinance your mortgage. Nobody said doing smart financial things was going to be fun. But…when it’s all done and you’re making money or reducing your expenses that optimizes for personal enjoyment…that IS fun.

I can’t tell you how many times we have refinanced our homes. I would say it’s been well more than ten times. Each time I refinanced with a lower interest rate or a better loan term, I thought I could never do better. I have refinanced a lot, and every time, I did better. I don’t think I’ll ever beat the home loan I have now. I hope I’m wrong.

More than ten years ago, I discovered interest-only loans. In retirement, I wouldn’t want to have any other type of home loan than an interest-only loan. Why in the world would I want a principal and interest loan? Why would I want to move money from my retirement portfolio, earning 8.8% over the long haul, to pay off a loan that was charging me a much lower interest rate? I wouldn’t want to do that. However, if my home loan rate were equal to or higher than my investment earning rate, I wouldn’t want to borrow.

Pearl. Borrow baby, borrow.

Here’s another opportunity to take what I am saying out of context. Please don’t do that.

Bottom-line…I wouldn’t want to have my house fully paid for in retirement. I think that is a devastating financial strategy.

Some people will tell me they “sleep better” knowing their house is paid for. That is a euphemism for “I don’t want to have any risk whatsoever”.

Some people prefer annuities because the return is guaranteed. No risk. A guaranteed rate of return will always be lower, over the long run, than a market return. How is that? The person/entity giving you the guarantee is earning a market return. How could they take their profit and still give you a market return when they are only making a market return? They couldn’t.

I “sleep better,” knowing that money that could have been sitting in my home equity earning exactly NOTHING is, in reality, gaining 8.8% on average each year. I sleep so soundly that I rarely get out of bed before 8 a.m. I know some folks have a full day’s worth of chores done by that time of day… but then I don’t do chores.

Pearl. The secret to a successful financial result? Compounding.

My net worth has benefited from the most significant financial benefit anybody can have: compounding. I’ve earned 8.8% over a long period of investing, 23 years. The longer I earn that rate of return, the bigger the investment account. That’s the benefit of compounding.

Pearl. Free! This is one of the most important concepts I am sharing today.

Whoa! This one is really important!

I consider most things that I buy nowadays to be FREE. Did Randy say free? Yes, he did. I don’t pay all that much attention to the price of anything, nor does it influence my decision to buy something.

I’m not as young as I was when I retired in 2002, and I don’t have as long to live in 2025 as I did then.

I will never spend all my money sitting in my investment accounts. I invested that money so that Carol, my family, and I could enjoy it. I told you a thousand words ago that money alone isn’t worth anything. Money is to be spent. Money is to be enjoyed. You can enjoy it, your family can enjoy it, or anyone else you decide to share your financial wealth with can enjoy your money. If the money isn’t enjoyed by you or someone, then you were an idiot to bust your butt earning the money in the first place.

Free? Randy, please explain further.

I told you that I consider the stuff I buy today to be free. If I don’t spend my retirement money, it will be sitting over at Vanguard when they start dumping dirt on my casket. How about an example of “free”?

Most people have some money saved in retirement. I’m going to say that money can be divided into two buckets. The first bucket of money is reserved for your living expenses until you die. Your living expenses would be your housing, medical expenses, food, utilities, insurance, taxes, etc.

Importantly, the second bucket contains your remaining retirement funds, which you will, in all likelihood, never spend. What good is money you will never spend?

I believe I can afford to take some of the money from that second bucket and SPEND IT NOW! I don’t need money from bucket #2 to live on because my “live on” money comes from bucket #1.

Carol and I are going to New York City in December. We do that once or twice every year. We will be staying in a suite in New York City. We will dine at the best restaurants and go to the best Broadway plays. All of this stuff is free! The money comes from bucket #2. Remember, bucket #2 is holding the money I will never spend! If I don’t spend some or even all of the funds from bucket #2, then I worked for nothing.

How about another example? You’ve got the time, right? Let’s say you have $2,500, $25,000, or $250,000 in your bucket #2 of retirement investments that you NEVER expect to spend. Where will that money go when you die? To whomever is a beneficiary of your will. When will you die? You don’t know.

Now, let’s say you don’t die for one year to fifty years. Why wait to spend the amounts of money listed above that you NEVER expect to spend? I recommend you spend that money on yourself or your heirs NOW. They’ll likely enjoy spending that $2,500, $25,000, or $250,000 now more than when you die in X amount of years. If you spend some or all of that bucket #2 money now, the stuff you buy will be FREE!! It didn’t cost you a thing. The money you spend now with this strategy is money you were never going to spend anyway. This is a new concept to some. Take a moment to understand the idea fully.

Pearl. What good is money if you don’t spend it?

If we don’t spend the money we’ve earned with a solid retirement financial plan, the money will be useless to us. Does it matter what a new iPhone costs or a basketball ticket, a hotel, or a restaurant?

Carol and I were not always in this position. Our wedding costs were $500 in total. We paid for the entire thing. We took out a $200 bank loan to cover that $500 expense for our wedding. This was the total cost of our wedding, including our rehearsal dinner and after-party.

We were practicing “Die with Zero” principles at age 23! We spent all our money, our entire net worth, plus $200, just for a big party! We were optimizing for personal enjoyment and creating memory dividends. We knew those costs would be insignificant compared to the money we would have later in life.

When we were first married, we bought a king-size mattress and slept on the floor for the first year. We did that until we could afford the headboard and box springs we wanted. We got our China one dish at a time by making a $10 or maybe a $25 deposit into a bank account. We still have that fine China today. It looks great.

Pearl. This is a message about having a plan and getting results. It is not a message about money.

I don’t want anyone to think my life is only about money. Today’s newsletter is a message about the results I have achieved from my retirement financial portfolio. This particular newsletter is meant to talk about money.

Money is a supporting character in life. I would much rather have money than not. Money can create comfort. Money can create freedom. I would much rather have a life that is comfortable and offers freedom. That’s the value of money.

A message for all ages.

If you are in your 20s or 30s, you might still consider this a missive from some old guy. If you are in that age range and think that my retirement lifestyle, which began in my 50s, is a lifestyle you might want to emulate, then you need to have a plan now. You can take elements of my plan or any other plan, but you need a plan. You need to work on that plan daily. You can’t deviate. You can’t market time.

If you’re young and poor, you can still save 25 bucks a week for the rest of your life. If you do, then you will have a healthy chunk of change to help you enjoy your retirement. Don’t think you can save $25/month? I could walk into your household tonight and find much more than what you waste every week. You can’t blame anybody else for not having a plan.

If you are in your 40s or 50s, I hope you’ve been working on a plan for a while. If you haven’t, you need to stop what you’re doing immediately, get a plan, and work that plan 24/7.

If you are in your 60s or older, I hope you’ve enjoyed reading what I have shared. You’re in your own boat now. Your boat might be much smaller than mine, or it might be much larger. Whatever boat you’re in, I hope you’re comfortable, making memories, and sailing in whatever direction you like.

Pearl. Money has a declining utility over time.

Regardless of age, older folks need to understand that money has a declining utility over time. Cash is less valuable to you when you are 80 than when you are 30. You could do much more with money at age thirty than when you are older.

If you can’t use your money today and still have several years of life expectancy, consider giving money to others. They, in most cases, CAN use that money today. Then, at least, you will get the psychic value of seeing someone enjoy your money.

Kids!

We have three children, in their late 40s and early 50s today. We were a “pay for performance” family. If you performed, you got paid. We decided that paying for our children’s college education would be our financial contribution to them. I (also Carol!) paid 12 years of tuition for our three kids to attend UCLA. What did we get out of doing that? Lots of sweatshirts and T-shirts, and a profound admiration for our kids’ achievements.

Luckily for everyone, they each graduated in four years! Then we gave them all a lovely graduation gift and sent them on their way financially. They have all done well, and we are exceedingly proud of them.

Pearl. Everybody’s older. What is the next step?

Now we are older. The kids are older. Should we give them money now or wait another 20 years (hopefully!) for them to get some of our money upon our earthly exit? They will all be approaching seventy, then. At that point, THEY will be too old to enjoy skiing as much as they could when they were forty. We’ve come up with an excellent mid-range solution.

We don’t have to GIVE them any money right now, but we will. However, we can tell them right now how much they will be GUARANTEED (second-to-die life insurance) to get when Carol and I take the final checkered flag. Then they can spend the money they were planning to need for retirement NOW, knowing that our gifts will replace that money.

These may be “out of the box” ideas for you. Don’t take what I’ve said out of context.

I cautioned at the beginning that I hope no one takes anything that I’ve said out of context to support a personal point of view.

I have been 100% honest with you. I believe I have been more candid on these topics than virtually any source you might have from family, friends, or news agencies. Everything I’ve shared is 100% accurate and truthful.

I hope you didn’t think I bragged. I did all of this, so I guess I am justified in telling you how it all came down.

Pearl. Why share? So someone might get the results I’ve gotten.

A good friend of mine recommended that I say, “I earned 13.2%. It was a good year,” and leave it at that. I don’t roll that way. I want to help people. I don’t expect compensation other than maybe a thank you somewhere down the line.

Someone who reads this might use my ideas or modify them to make them their own. When they do, there is an excellent chance they will be able to optimize their lives for personal enjoyment. There is an excellent chance they will create many lasting memory dividends. Memories are much more valuable than having a lot of money in the bank and no memories.

I hope you don’t think I am a financial stud. I am not. I have more money today than when I retired because I wasn’t smart enough to spend it until now. Maybe I worked too long. I’m trying to improve in this area.

I got to this point by listening to other people. I followed the advice of William Bernstein. I continued to practice the principles offered up by Bill Perkins, who wrote Die with Zero.

Was I lucky? I don’t think so.

Carol and I have been lucky in several vital areas. At the same time, I’ve found that the better our preparation, the more fortunate we were. I’ve heard it said that it’s better to be lucky than good, and I want to be both. We had a plan. We worked the plan. The plan is working for us.

Thanks for reading.

That’s it. Thanks for tuning into my 2025 retirement “Financial Plan of a Lifetime”. I know you’re busy. Maybe you’re thinking there’s a lot of good stuff in here. You’ll act on things when your life slows down. We all know what that means. My recommendation? Act now.

Pearl. Predictions for the future.

One last thing. What is my projection for the future of stocks and bonds?

I have no frigging idea. That’s why I am not a market-timer.

You would have to think the market is ready for a pause since it’s been doing so well. That’s what people said five and ten years ago.

On the last day of my fiscal year (October 10, 2025), the market (S&P 500) dropped 2.71%! That reduced my FY results from 15.7% to 13.2%. The market goes up and the market goes down. That’s why I only look at market results every month or two.

I hope I haven’t made my “Financial Plan of a Lifetime” sound as if it’s easy to pull off. It’s not. But if you have the right plan, as I do, the odds will be dramatically in your favor.

Then, when the market does do well, you just need to know how to enjoy the rewards your good planning gave you.

I know this about the stock and bond markets: The markets will go up and down in the future. I don’t know when they will go up or down. I don’t want to be out of the market when it goes up. That would be stupid, painful, and financially hurtful.

See ya next year on this subject.

Randy said all of this. He don’t do chores. He’s got a good wife. She don’t eat much and she don’t spend much money…but she does do chores. We enjoy living in our modest seaside cottage and traveling the world.

Yes, Randy said all of this…and Carol agrees!